Policy Pro (Case study in progress)

Credit Karma's insurance marketplace has proven revenue-positive, prompting leadership to double down with a focus on longer-term innovation.

In late 2025, I was tapped to lead an innovation pod exploring horizon 2+ initiatives — engagement-first bets not expected to drive near-term revenue, but designed to cement Credit Karma as the go-to destination for insurance shoppers.

The problem

Credit Karma's insurance marketplace was working. It made money. Leadership wanted more of it.

But two cracks were showing.

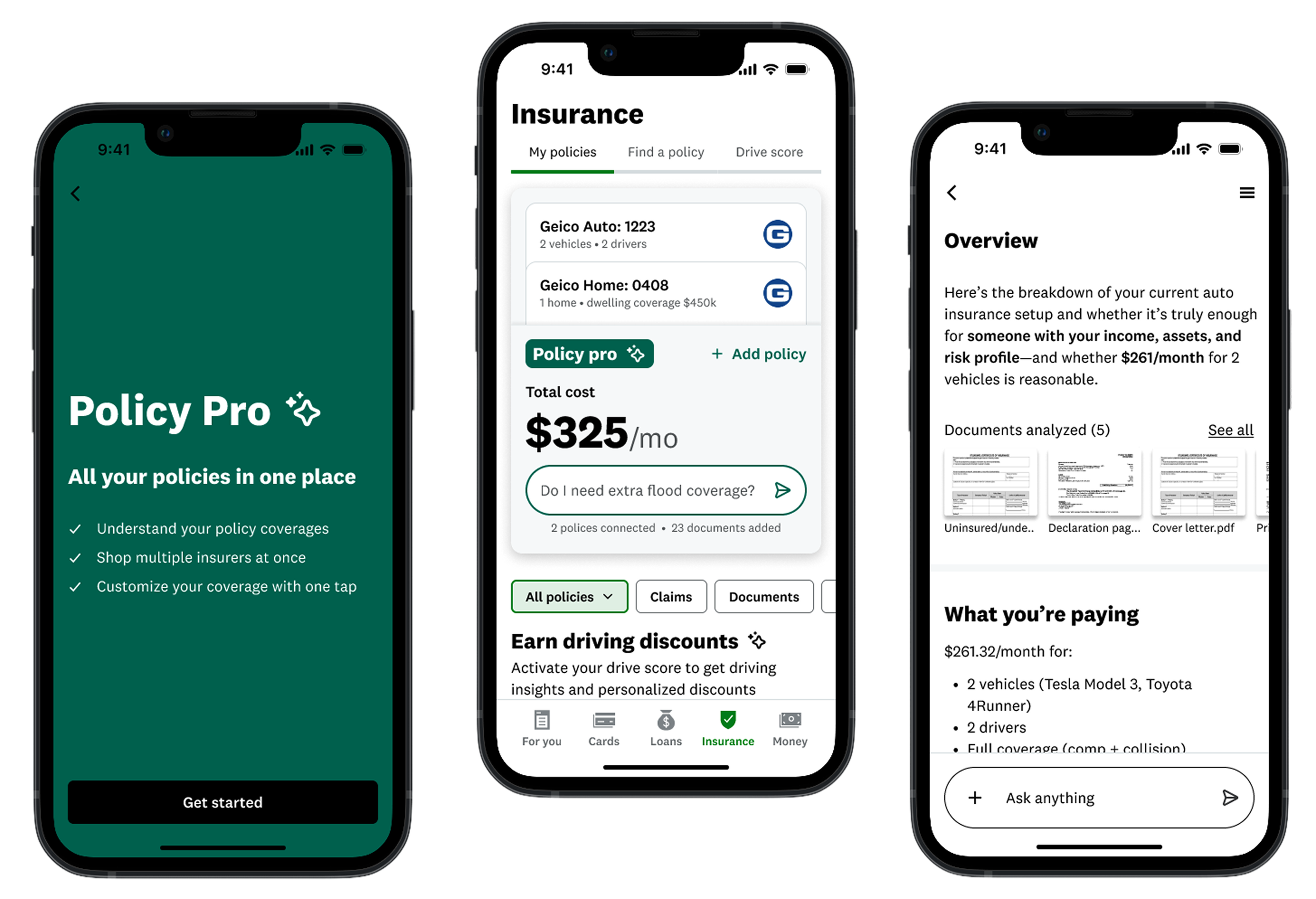

When Credit Karma acquired Zendrive in 2024, we shipped a usage-based insurance product called Credit Karma Drive. Smart bet on the future of auto insurance. The problem: if a member landed on the insurance surface and didn't want to opt into UBI tracking, the surface had nothing else for them. It was a dead end.

The other crack was Connected Policy — the feature that lets members link their actual insurance policy to Credit Karma. The engineering lift to build it was real. The value proposition was not. Members connected their policy, got a few flat insights, and never came back.

So the question wasn't should we expand insurance. It was what would actually pull members back to this surface between purchase moments.

The challenge

Our goal was to grow engagement on the insurance surface by building experiences that solve real problems for members between insurance purchases.

Hypothesis (high level)

We believe that…

Solving real insurance problems for our members

will result in…

Increased return visits to the insurance surface

Increased insurance conversions at renewal

which will ultimately…Grow revenue from Credit Karma's insurance marketplace

My role

I led the innovation pod from an ambiguous brief through a validated vision and a sequenced path to ship.

My scope included:

Reframing the problem from a feature gap to a member confidence gap

Aligning a newly formed cross-functional pod through paired Foundation and Design Sprints

Leading generative and evaluative research in close partnership with Product Research

Translating the vision into a sequenced set of in-market experiments with the PM

Building an internal Claude tool that kept BD, Partner Success, and design aligned on the throughline from vision to shipped work

While I owned design direction, success depended on influencing leadership's appetite for Horizon 2+ work and building alignment across Product, Engineering, Research, BD, and Partner Success.

Understanding the problem

Approach

We started where the answers actually live: talking to members.

Before we wrote a single brief, I ran a Foundation sprint to align the team on the long-term bet, then a traditional design sprint to pressure-test our riskiest assumptions. In between, we did contextual inquiry — sitting with members as they navigated their declarations pages, renewal emails, and insurer apps.

The temptation in innovation work is to start with technology. We started with confusion. What did members not understand? What were they afraid to ask their insurance company? Where did they feel stuck?

What we learned

A few patterns held across nearly every interview:

Members don't know if they have the right coverage. Most read their policy once at signup and never again.

Renewal is a black box. Premium goes up. Members don't know why. Most just pay it.

Insurance language is hostile. Comprehensive vs. collision, declarations pages, endorsements — the vocabulary alone keeps people from engaging.

The shopping moment is rare. The wondering moment is constant.

I built interview snapshots after each session, used the Continuous Discovery framework to keep us honest about which assumptions we'd actually validated, and mapped findings onto an opportunity solution tree.

The tree became the artifact we used in every leadership conversation. It made the bets legible.

A few patterns held across nearly every interview:

Members don't know if they have the right coverage. Most read their policy once at signup and never again.

Renewal is a black box. Premium goes up. Members don't know why. Most just pay it.

Insurance language is hostile. Comprehensive vs. collision, declarations pages, endorsements — the vocabulary alone keeps people from engaging.

The shopping moment is rare. The wondering moment is constant.

I built interview snapshots after each session, used the Continuous Discovery framework to keep us honest about which assumptions we'd actually validated, and mapped findings onto an opportunity solution tree.

The tree became the artifact we used in every leadership conversation. It made the bets legible.

Developing a product vision

A vision that can't be tested is a deck. We needed to break Policy Pro into bets that could ship in weeks, not quarters.

We landed on three:

Connected Policy Lite. Strip the original Connected Policy down to the data we actually needed to assess coverage and cost. Lower the integration cost. Make the value visible in the first session.

AMA chat experiment. A conversational surface seeded with starter prompts. The point wasn't to ship a chatbot — it was to learn, at scale, what members actually want to ask about their insurance.

A Claude-powered internal prototype. This one cut sideways. I built a prototype to help our own BD and partner success teams have better conversations with insurance partners — surfacing what's live, what's in production, and how each shipped feature ties back to the vision. Internal alignment is part of the work. The throughline only holds if everyone touching it can see it.

Each bet was designed to feed the vision while standing on its own. If the vision shifted, we'd still have learned something. If it held, we'd have receipts.

Developing a product vision

Outcome: 8% increase in activations

With the connected policy light set up, we saw a sharp increase in lite activations – which means we can deliver more compelling and personalized product experiences.

Reflection

This project set the foundation for roadmap items for years to come. Although not perfect, the vision prototype acted as a north star for smaller product sprints that could incrementally deliver value to members over time.

Leveling Up Other Designers

During this period, all designers at Intuit were asked to learn Claude code and Github. As mentioned earlier in the case study, I led efforts to assist other designers on the insurance vertical in setting up their Github accounts and contributing to shared projects.